By Riverfront Investment Group

2020 began with the signing of the Phase One trade deal between the US and China. Investors cheered the agreement, propelling global equity markets higher and the S&P 500 to new highs as it signaled a halt to the tariffs that stunted global growth in 2019. With the Federal Reserve’s rate cuts on hold, the trend continuing to rise, and the crowd not at an extreme, markets appeared to have more room to run.

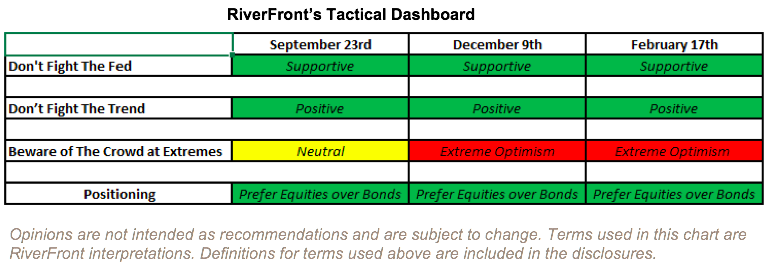

However, the recent outbreak of the coronavirus has caused some investors to question whether the 11-year bull market may be at risk, making it a good time to revisit our three tactical rules, “Don’t Fight the Fed,” “Don’t Fight the Trend,” and “Beware of the Crowd at Extremes.” Upon review, we have concluded that our tactical rules continue to indicate that the conditions are in place for equity markets to advance over the next three months. The chart below shows how coronavirus fears have brought the three rules back to September 2019 levels (see Weekly View from 9/24/19).

DON’T FIGHT THE FED: Investors should not go against the policy guidance of central bankers in the US or abroad.

The Federal Reserve started the new year firmly on hold after cutting interest rates three times last year and growing its balance sheet for the first time since 2014. Since August 2019, the Fed has committed to support the economy through a $406.8 billion balance sheet expansion, cut interest rates twice for ‘insurance against ongoing risks’ according to Jerome Powell, and counteracted an inverted 3-month/10-year yield curve. Despite the Fed’s rate cut campaign being on hold, we believe that the Fed will continue to react accordingly to maintain the expansion. For example, the Fed recently stepped in and increased its balance sheet by nearly $15 billion over the last 3 weeks to offset the coronavirus’ impact, which briefly inverted the 3-month/10-year yield curve again.

While the Fed has been able to use monetary policy to control interest rates, it has not been able to hit its inflation target of a sustained 2%, causing Chairman Powell to have a dovish tone to his prepared statement after the January 29th meeting. The bottom line is that we believe the Fed will continue to hold interest rates at low levels to achieve its 2% target, which in turn provides investors access to low cost financing, the ability to refinance mortgages, and more discretionary income. The Fed is on the investor’s side, in our view.

Internationally, the European Central Bank (ECB) and the Bank of Japan (BOJ) continue to also have supportive monetary policies to mitigate the impact of their slowing economies. Like the Fed, we believe that the ECB and BOJ will do whatever it takes to maintain economic stability, and small fluctuations in balance sheet size are just a result of general operating procedures. For its part, the People’s Bank of China, concerned over the coronavirus’ impact on its economy, has also engaged in rate cuts, liquidity injections and more accommodative loan terms just in the last few weeks. Overall, we believe that global central banks are supportive and on the investor’s side.

DON’T FIGHT THE TREND: Investors should determine the direction and strength of the trend and adjust their investment decisions accordingly.

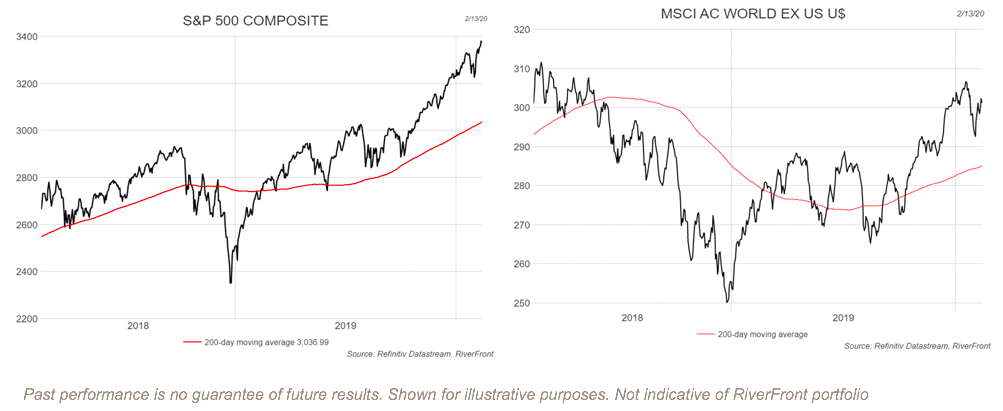

Currently the US primary trend, which we define as the S&P 500’s 200-day moving average, is rising at an annualized 18% rate as of February 17th. The trend is currently being calculated from May 3, 2019. Last year on May 3rd, the S&P 500 was sitting at 2945 which was only 15 points higher than the high made the previous September. The market would subsequently spend the next 40 trading days (nearly two months) before making a meaningful breakout to higher levels. This brief walk down memory lane helps us understand what to expect from the current trend over the next 3 months. If the S&P 500 trades sideways for the next 3 months the trend will peak at a 24% annualized rate and then fall to a much more sustainable rate of 15% annualized, in our view. We believe the important takeaway is that the trend is positive and will remain positive for the foreseeable future in the US.

The international primary trend, which we define as MSCI All Country World ex-US index’s (ACWX) 200-day moving average, is expected to follow a similar pattern to its US counterpart albeit at a slower pace. The international trend is rising at a lower 6% annualized rate and continues to have less support than the S&P 500 as international markets are trading only slightly higher than their May 2019 level. However, now that some of the trade headwinds that weighed on international markets last year have subsided and international markets have begun to move higher, we expect the trend to remain a positive for investors. Over the next month, the international trend will accelerate to a 11% annualized rate if ACWX trades sideways, which means the trend is supportive for investors to take on additional equity exposure, in our opinion.

BEWARE OF THE CROWD AT EXTREMES: Analyze sentiment by determining if it is sustainable at current levels. If sentiment is identified to be unsustainable, then as investors we must be willing to lean in the other direction and be prepared to act aggressively once the condition changes.

Ned Davis Research’s (NDR) Weekly Crowd Sentiment Poll (see chart above) has recently moved into the extreme optimism zone after falling into the neutral zone after the coronavirus outbreak. The coronavirus brought the potential of slowing global growth back to the forefront due to China being the epicenter of the outbreak and their outsized impact on the global economy. We believe the pullback of the sentiment indicator represented an opportunity to continue purchasing risk assets. Stock market gains always involve pullbacks, and the S&P was up 9.1% in the 4th quarter and an additional 3.4% to start the year through January 17th . We believe that equity markets needed a breather, and the coronavirus provided it for about two weeks before resuming their climb higher. As the pace of coronavirus cases slowed, worries turned to hopes. Sentiment continues to be supported by a strong labor market, with unemployment registering just 3.6%, and a better-than-expected 4th quarter earnings season. However, if the coronavirus becomes a pandemic, crowd sentiment could deteriorate further, and we would look at this as a potential buying opportunity. We believe the current crowd sentiment reading is supportive for equities to rally given it is well below previous extremes.

THE FINAL VERDICT:

We believe the Fed and central banks around the world are signaling that they will do whatever is needed to continue the expansion. Central bankers’ willingness to aid the expansion creates a supportive backdrop for equity performance around the world. We believe that the combination of a rising trend and neutral sentiment increases the odds of above-average equity returns over the next 3 months. Our three tactical rules continue to give a bullish signal and our portfolios are tilted towards having more equity exposure.

This article was written by the team at RiverFront Investment Group, a participant in the ETF Strategist Channel.

Important Disclosure Information

The comments above refer generally to financial markets and not RiverFront portfolios or any related performance. Past results are no guarantee of future results and no representation is made that a client will or is likely to achieve positive returns, avoid losses, or experience returns similar to those shown or experienced in the past.

Information or data shown or used in this material is for illustrative purposes only and was received from sources believed to be reliable, but accuracy is not guaranteed.

In a rising interest rate environment, the value of fixed-income securities generally declines.

Technical analysis is based on the study of historical price movements and past trend patterns. There are no assurances that movements or trends can or will be duplicated in the future.

Investing in foreign companies poses additional risks since political and economic events unique to a country or region may affect those markets and their issuers. In addition to such general international risks, the portfolio may also be exposed to currency fluctuation risks and emerging markets risks as described further below.

Changes in the value of foreign currencies compared to the U.S. dollar may affect (positively or negatively) the value of the portfolio’s investments. Such currency movements may occur separately from, and/or in response to, events that do not otherwise affect the value of the security in the issuer’s home country. Also, the value of the portfolio may be influenced by currency exchange control regulations. The currencies of emerging market countries may experience significant declines against the U.S. dollar, and devaluation may occur subsequent to investments in these currencies by the portfolio.

Foreign investments, especially investments in emerging markets, can be riskier and more volatile than investments in the U.S. and are considered speculative and subject to heightened risks in addition to the general risks of investing in non-U.S. securities. Also, inflation and rapid fluctuations in inflation rates have had, and may continue to have, negative effects on the economies and securities markets of certain emerging market countries.

Stocks represent partial ownership of a corporation. If the corporation does well, its value increases, and investors share in the appreciation. However, if it goes bankrupt, or performs poorly, investors can lose their entire initial investment (i.e., the stock price can go to zero). Bonds represent a loan made by an investor to a corporation or government. As such, the investor gets a guaranteed interest rate for a specific period of time and expects to get their original investment back at the end of that time period, along with the interest earned. Investment risk is repayment of the principal (amount invested). In the event of a bankruptcy or other corporate disruption, bonds are senior to stocks. Investors should be aware of these differences prior to investing.

It is not possible to invest directly in an index.

Standard & Poor’s (S&P) 500 Index measures the performance of 500 large cap stocks, which together represent about 80% of the total US equities market.

MSCI ACWI ex USA Index captures large and mid cap representation across 22 of 23 developed markets (DM) countries (excluding the US) and 23 emerging markets (EM) countries.

Definitions: Don’t Fight the Fed – ‘Supportive’ means the Fed’s monetary policy regarding inflation and employment is in what we believe based on our analysis to be the investors’ best interest; ‘Against’ means the Fed’s monetary policy, in our view, is going against the investors’ best interest; ‘Neutral’ means the Fed’s monetary policy is neither supportive or against the investors’ best interest in our view. Don’t Fight the Trend – Terms correlate to the 200-day moving average as it relates to the equity indexes: ‘Positive’ means that the trend is rising, ‘Flat’ means the trend is flat, ‘Negative’ means the trend is falling. Beware the Crowd at Extremes – Terms correlate to the NDR Crowd Sentiment Poll and its measurement of Extreme Optimism (Bearish), Neutral, or Extreme Pessimism (Bullish).

RiverFront Investment Group, LLC, is an investment adviser registered with the Securities Exchange Commission under the Investment Advisers Act of 1940. Registration as an investment adviser does not imply any level of skill or expertise. The company manages a variety of portfolios utilizing stocks, bonds, and exchange-traded funds (ETFs). RiverFront also serves as sub-advisor to a series of mutual funds and ETFs. Opinions expressed are current as of the date shown and are subject to change. They are not intended as investment recommendations.

RiverFront is owned primarily by its employees through RiverFront Investment Holding Group, LLC, the holding company for RiverFront. Baird Financial Corporation (BFC) is a minority owner of RiverFront Investment Holding Group, LLC and therefore an indirect owner of RiverFront. BFC is the parent company of Robert W. Baird & Co. Incorporated (“Baird”), a registered broker/dealer and investment adviser.

Copyright ©2020 RiverFront Investment Group. All Rights Reserved. 1088735